AMA Group’s H1 FY2023 report shows the organisation has improved its financial standing despite posting a net loss of $27.2 million – a 43 per cent gain over the $48.1 million net loss posted in H1 FY2022.

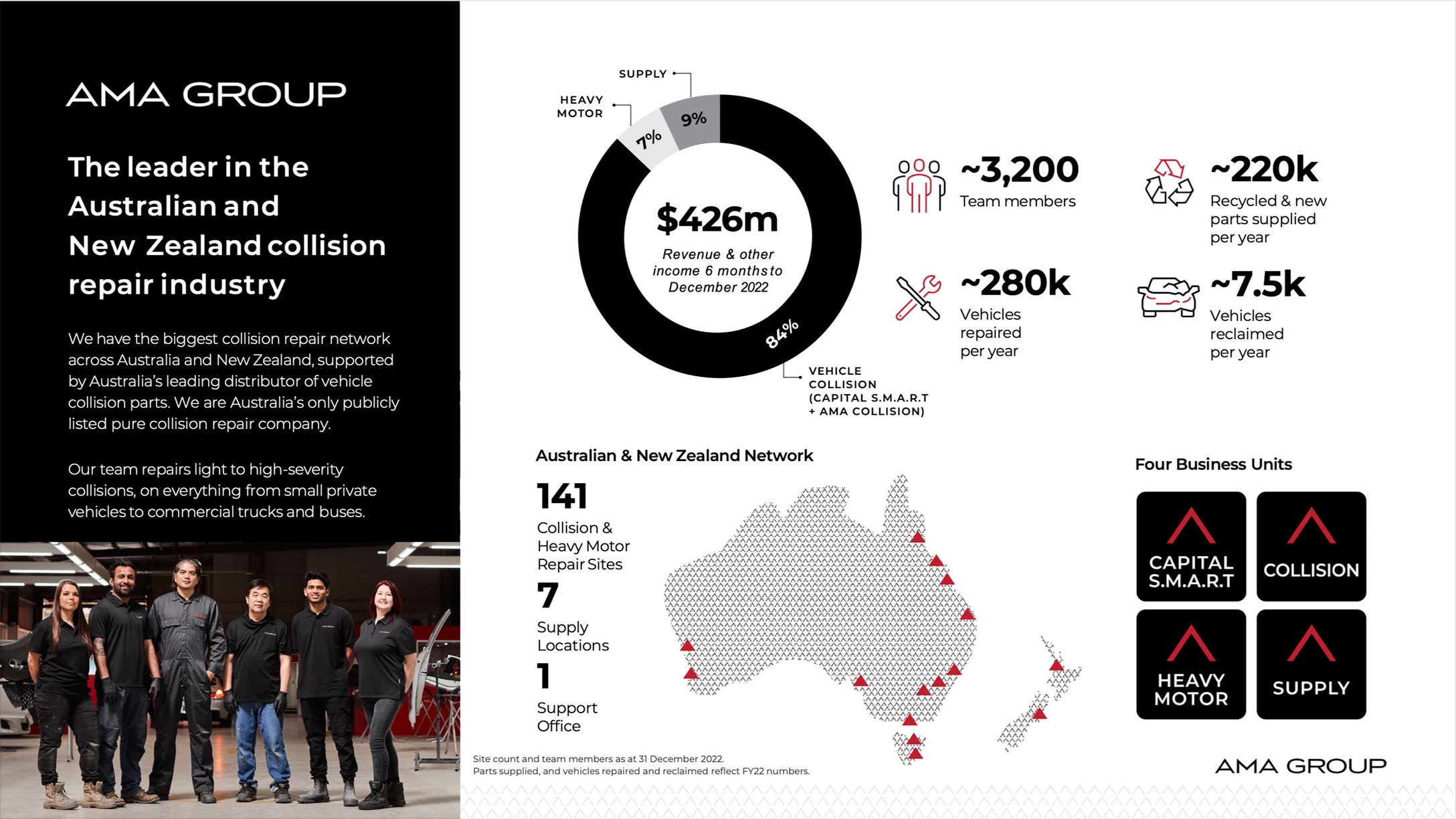

Revenue remained relatively stable at $426.2 million, a two per cent improvement over the corresponding period last year.

The company also posted a 502 per cent improvement in normalised EBITDA (post-AASB 16) of $25.3 million, versus $4.2 million recorded for H1 FY2022.

No dividend will be paid for the period.

According to AMA, the gains reflect improved insurer pricing – including interim Capital S.M.A.R.T pricing from October 2022, a transition year where volumes were impacted through:

- Pricing negotiations

- Consolidation of scarce labour to fewer, larger facilities with profitable work provision

- Improved productivity and reduced lead times

- Increased parts disintermediation through supply operations, and

- A reset of the business’s fixed cost base to reflect operational requirements.

The report also noted:

- A $4.6 million non-cash impairment expense – a combination of right-of-use assets and leasehold improvement / equipment

- A $16.7 million prior period impairment against right-of-use assets (leases)

- Leasehold improvements, and

- Plant and equipment for sites planned for closure, hibernation, or consolidation with other sites.

Finance costs also increased, but 64 per cent of debt is hedged from October 2022 through to maturity at less than 5.5 per cent all-in interest cost.

Cash and cash equivalents were listed at $33.3 million, a 36 per cent drop on the $52.2 million posted for H1 FY2022, with the company saying it “maintains a strong financial position with sufficient cash reserves for the FY2023 transition year”.

AMA said operating cash outflow of $4.1 million was a substantial improvement from $22.8 million in H1 FY2022, reflecting improved EBITDA performance, a $15.3 million tax refund received under ATO carry-back rules, $8.9 million of operating cash flow invested in building ACM Parts’ inventory range, and the Fluid Drive sale proceeds of $2.4 million.

According to AMA, net operating cash flows reflect the transition period back to profitability following revised commercial outcomes and the site optimisation programme, with nine leases exited in the current period resulting in lower rental payments ($2 million per annum) going forward and $1.4 million cash outflow associated with making goods on these leases in H1 FY2023.

The Vehicle Collision Repairs division showed strong improvement in operating performance, reflecting impacts of improved pricing and consolidation of sites and labour, offset by continued inflationary pressures. Revenue and other income were $372.7 million, up from $357.6 million in H1 FY2022 despite a four per cent drop in repair volume, while normalised EBITDA was up at $20.7 million compared to $7.2 million last year.

“We’ve now seen improving financial results for the past three quarters, reflecting both cost management initiatives – including network optimisation – and the commercial activities around pricing and unprofitable work,” said Geoff Trumbull, Chief Financial Officer of AMA.

According to Trumbull, the benefit of these initiatives is yet to be fully realised.

“The Group expects to see further transition in operating cash flows across the year as there is a lag in receiving some of the benefits of the site optimisation programme as rents roll off later than site exits, commercial pricing given lead times on repairs and collections, and the revised BASF paint arrangements,” he said.